Key Takeaways:

- Fintech companies face growing pressure from stricter regulations, rising cyber threats, AI governance risks, and increasing infrastructure costs, making sustainable growth harder to achieve without operational resilience.

- Fintech startups and scaleups can reduce regulatory and security risks by adopting compliance-by-design, zero-trust security architecture, RegTech automation, and explainable AI frameworks from the product development stage.

- Prioritizing challenges through a fintech severity matrix, measurable 90-day milestones, and specialist partner ecosystems helps companies improve scalability, compliance readiness, and capital efficiency.

- As fintech matures, long-term market leaders will be defined by their ability to integrate compliance, cybersecurity, AI governance, and infrastructure resilience into a scalable operating model.

________________________________________________________________________________________

The fintech industry is expanding rapidly, with the global market valued between $305 billion and $340 billion in 2023 and projections approaching $1 trillion by 2032. But growth has brought new challenges. Fintech companies today must manage stricter regulations, cybersecurity threats, rising customer acquisition costs, infrastructure dependencies, and increasing demands for trust and compliance. Building a strong product alone is no longer enough.

The companies that succeed are rarely the ones relying only on funding or speed. They are the ones that identify fintech challenges early, reduce operational risk, and adapt faster than competitors. This guide explores the 10 most important fintech industry challenges in 2026, practical solutions being used to address them, and how fintech leaders can prioritize what to solve first.

The Three Macro Factors Making Every Fintech Challenge Harder in 2026

Before looking at individual fintech challenges, it is important to understand why the entire operating environment has become more difficult:

The end of cheap capital. Venture funding for fintech fell nearly 50 percent from its 2021 peak. The era of growth-at-all-costs is over. Investors now require a clear path to breakeven, defensible technology, and a credible regulatory strategy before writing checks. This changes how every challenge must be approached: there is no longer a funding cushion to absorb strategic mistakes.

Regulatory tightening across every major market. The EU AI Act became effective in 2026. PSD3 is reshaping open banking in Europe. The US Consumer Financialulatory Compliance Across Multiple Jurisdictions Protection Bureau has intensified scrutiny of fintech lending practices. Markets that were previously light-touch are introducing licensing frameworks. Compliance has moved from a back-office function to a core business risk.

AI disruption on both sides of the equation. AI is simultaneously the most powerful tool available to fintech companies and the source of a new category of risks. Deepfake-enabled fraud, synthetic identity attacks, and model bias in credit decisions are problems that did not exist at scale five years ago.

These three forces sit underneath every challenge described in this guide.

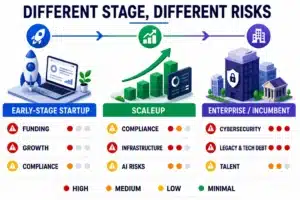

Challenge Severity Matrix: Where to Focus First

Fintech challenges do not impact every business at the same intensity. A startup managing early traction faces a different risk profile than a scaleup expanding operations or an incumbent modernizing legacy systems.

The matrix below highlights which challenges demand immediate attention based on business maturity, helping teams prioritize resources more strategically.

| Challenge | Early-Stage Startup | Scaleup | Enterprise / Incumbent |

| Regulatory Compliance | High | Critical | Critical |

| Cybersecurity and Fraud | Medium | High | Critical |

| AI-Specific Risks | Low | High | High |

| Third-Party API Costs | Medium | High | Medium |

| Legacy Tech and Technical Debt | Low | Medium | Critical |

| Funding Constraints | Critical | Medium | Low |

| Customer Acquisition and Retention | High | High | Mediumlatory Compliance Across Multiple Jurisdictions |

| Talent Shortage | Medium | High | High |

| Embedded Finance and BaaS Dependencies | Medium | Critical | Low |

| International Expansion Barriers | Low | High | High |

Core Insights: Priorities shift as fintech companies evolve. Early-stage firms often struggle with funding and customer growth, while scaleups face mounting compliance and infrastructure pressure. Enterprises, on the other hand, must balance modernization, cybersecurity, and operational complexity at scale.

The 10 Biggest Fintech Challenges and How to Solve Them

The fintech operating environment in 2026 is defined by heightened regulatory scrutiny, rising security risks, changing capital dynamics, and increasing infrastructure complexity. The following challenges represent the areas most likely to influence product scalability, operational resilience, and long-term growth.

For each challenge, we have examined:

- What the challenge involves,

- Why is its impact intensifying in 2026,

- The practical measures fintech organizations can take to address it.

Challenge 1: Regulatory Compliance Across Multiple Jurisdictions

What is it?

Fintech companies operating across borders face a fragmented regulatory environment where the rules change not just by country but by product type, customer segment, and transaction volume.

| Geography | Regulatory Requirements |

| UK customers | FCA requirements |

| US transactions | FinCEN rules, state money transmitter licenses, and CFPB guidance |

A payment company serving UK customers faces FCA requirements. The same company processing US transactions needs to navigate multiple regulatory frameworks simultaneously.

Why does it matter more in 2026?

The regulatory environment in 2026 is markedly more enforcement-oriented, with supervisory authorities increasing scrutiny across AML, consumer protection, licensing, and operational risk obligations.

Recent enforcement actions include:

- Block (Cash App parent): $80 million fine by US state regulators

- Revolut: 3.5 million euro fine

- Monzo: 21 million pounds fine by the FCA

These are not small operators making amateur mistakes. They are well-funded companies with sophisticated compliance teams. The enforcement trend reflects heightened expectations around governance, risk controls, and regulatory readiness, even among scaling fintech organizations.

The EU AI Act adds a new compliance layer specifically for fintechs using automated decision-making in credit scoring, fraud detection, or underwriting. High-risk AI systems now require:

- Documentation

- Human oversight mechanisms

- Bias testing before deployment

How to solve it?

The companies managing compliance best are not the ones with the biggest legal budgets. They are the ones who built compliance into the product architecture from the start.

Recommended compliance measures include:

- Adopt compliance-by-design: Make regulatory requirements a product requirement, not a post-launch checklist. When KYC flows, transaction monitoring logic, and data residency architecture are designed with embedded regulatory controls, both compliance costs and market expansion friction decrease significantly.

- Deploy RegTech infrastructure: Tools such as ComplyAdvantage and Flagright automate transaction monitoring, AML screening, and sanctions list checks at scale. For growing fintech organizations, these capabilities support compliance functions that can scale alongside transaction volume.

- Leverage regulatory sandboxes: Available in the UK, EU, Singapore, and other markets, regulatory sandboxes allow early-stage companies to test products under real operating conditions with supervisory guidance before full licensing. The FCA sandbox alone has launched over 100 companies that would otherwise have spent months navigating licensing uncertainty.

- Designate a compliance engineer: Beyond traditional compliance functions, fintech companies increasingly require professionals who understand both regulatory requirements and how to translate them into technical controls. Although this role remains specialized and costly, it represents one of the most strategically valuable hires for scaling fintech organizations.

Challenge 2: Cybersecurity Threats and Data Breaches

What is it?

Financial data remains one of the highest-value targets within the cybercrime ecosystem. Fintech companies, by definition, operate at the intersection of financial transactions and digital infrastructure, making them particularly attractive targets for attackers seeking high-value returns.

Why does it matter more in 2026?

The cybersecurity threat surface has expanded faster than many security teams have adapted.

| Cybersecurity Indicator | Impact |

| Average global data breach cost | $4.88 million |

| Projected cybercrime losses targeting financial services (by 2027) | $24 trillion |

The 2024 Evolve Bank breach, which exposed data across multiple fintech platforms relying on Evolve as their banking partner, demonstrated how vendor-level compromises can cascade across broader fintech ecosystems.

The nature of threats has also evolved significantly. Emerging attack vectors include:

- Synthetic identity fraud: Combining real and fabricated personal information to bypass traditional KYC controls.

- Deepfake-enabled verification attacks: Audio and video manipulation used to circumvent biometric authentication systems.

- LLM-powered phishing campaigns: Personalized attack emails generated at scale with higher success rates.

- API exploitation: Attacks targeting open banking infrastructure are increasingly becoming a primary attack vector for fintech platforms.

How to solve it?

A zero-trust architecture should serve as the baseline security model for fintech organizations handling sensitive financial data. Under this model, no user, device, or service is trusted by default, including entities operating inside the network perimeter. Every access request is verified, and privileges are restricted to the minimum level required.

Recommended cybersecurity measures include:

- Deploy AI-powered fraud detection: Platforms such as Feedzai and Sardine analyze transaction behavior in real time to identify anomalies and prevent fraudulent activity before completion.

- Strengthen identity verification: Deepfake-resistant tools combining liveness detection, document forensics, and behavioral biometrics help mitigate synthetic identity fraud. Jumio and Onfido offer capabilities in this area.

- Establish a defined security testing cadence: Conduct quarterly penetration testing for critical systems, continuous API scanning, and annual red team exercises to assess evolving vulnerabilities.

- Maintain core security certifications: PCI DSS, SOC 2 Type II, and GDPR compliance should function as security architecture validation mechanisms, not checklist requirements.

Challenge 3: AI-Specific Risks

What is it?

The growing use of AI in financial services has introduced a new category of business risk. Unlike rule-based systems, AI models can create challenges related to bias, explainability, regulatory compliance, and model governance, particularly in high-impact financial decision-making.

Fintech companies are deploying AI across multiple functions, including:

| AI Use Case | Primary Application |

| Credit scoring | Lending decisions |

| Fraud detection | Transaction risk monitoring |

| Underwriting | Risk assessment |

| Customer service | Automated support |

| Investment recommendations | Portfolio guidance |

Each use case introduces risks that did not exist in rule-based systems.

Why does it matter more in 2026?

The EU AI Act classifies AI systems used in credit scoring and financial services as high-risk. This introduces mandatory,

- conformity assessments

- bias testing,

- human oversight requirements

- explainability documentation before deployment

For fintechs already operating AI models in these areas without documented governance, this creates a retroactive compliance challenge.

Algorithmic bias remains a material regulatory concern. A credit model trained on historical lending data will inevitably reflect historical lending patterns. If a model systematically underwrites applicants from specific demographic groups, fintech firms face both fair lending exposure and reputational risk once disparities become visible. Regulatory scrutiny in this area is increasing.

Model explainability also presents a practical operational challenge. When a customer’s loan application is declined by an AI model, most jurisdictions require a specific reason for that decision. Many deployed models cannot provide explanations in a format that satisfies regulatory standards. An adverse action notice cannot rely solely on model output.

How to solve it?

Recommended AI governance measures include:

- Implement explainable AI frameworks: Tools such as SHAP and LIME provide feature-level explanations for model decisions, supporting legally defensible adverse action notices.

- Establish recurring bias audits: Solutions such as IBM AI Fairness 360 and Fiddler AI enable ongoing monitoring for demographic disparities in model outputs rather than one-time validation during training.

- Develop EU AI Act readiness: Classify AI systems by risk tier and establish documented processes for conformity assessments, risk management, technical documentation, and human oversight for high-risk systems.

- Address specialized talent gaps: Data scientists with expertise in both machine learning and financial regulation remain limited. Where internal capabilities are insufficient, partnerships with firms specializing in regulated AI deployment may reduce implementation risk.

Building high-performing AI systems without the governance mechanisms required for deployment increasingly creates both regulatory and operational exposure.

Challenge 4: Rising Costs of Third-Party APIs and Infrastructure

What is it?

Most modern fintech apps do not build everything from scratch. Instead, they connect different pre-made digital tools together like Lego blocks. These tools are called APIs (Application Programming Interfaces).

For example, a new app might use Stripe to process card payments, Plaid to link to a user’s bank account, and ID.me to check IDs. This saves years of building time, but it means the fintech app is completely dependent on other companies to work.

Why does it matter more in 2026?

In the past, these API providers offered cheap rates to help new apps grow. Now, those providers are raising their prices to increase their own profits.

- The Margin Squeeze: Fintech companies that built their business plans a few years ago are suddenly facing much higher bills. For apps that handle thousands of daily transactions, a tiny increase in API fees can destroy their profits.

- The “All Eggs in One Basket” Risk: If you rely on just one provider for a core feature, they control your business. They can raise prices or change their rules overnight, and you are stuck paying whatever they ask because switching would take too much time and money.

How to solve it?

To keep costs low and retain control over your business, you need to plan ahead and build a flexible system.

- Ask for Hidden Discounts Early: Do not just pay the prices listed on a provider’s website. Most API companies have secret, cheaper pricing tiers for businesses that handle high volumes. Start negotiating before your traffic spikes, while you still have the leverage to walk away.

- Build an “Abstraction Layer” (A Backup Switch): Do not plug a third-party tool directly into the core of your app. Instead, build a digital “adapter” in your code. If you ever need to swap out one provider for a cheaper competitor, you only have to change the adapter.

- Know When to “Build vs. Buy”: Keep a close eye on your math. In the beginning, it is always smarter to buy (pay for an API). But once your app gets huge, it might actually be cheaper to build your own internal system. Constantly run the numbers to see where you can save money by taking control.

Challenge 5: Legacy Technology and Technical Debt

What is it?

For traditional financial institutions moving into fintech, legacy systems remain a defining operational constraint. Core banking infrastructure running on COBOL mainframes, in some cases operational since the 1970s, creates a significant agility gap relative to digital-native competitors.

For fintech startups, technical debt accumulates differently. Rapid iteration during early growth often produces architectural decisions that become increasingly expensive to reverse at scale.

Why does it matter more in 2026?

API-first fintechs integrate faster, deliver stronger customer experiences, and iterate at significantly higher speed than legacy-constrained institutions.

| Operational Reality | Impact |

| 70–80% of IT budgets are spent on maintaining legacy systems | Reduced capacity for product innovation |

| Faster iteration cycles among digital challengers | Increasing competitive pressure on incumbents |

For traditional banks, allocating the majority of technology spend to system maintenance has become increasingly unsustainable as digital competitors accelerate product delivery.

How to solve it?

Recommended modernization approaches include:

- Adopt the strangler fig pattern: For organizations unable to replace core banking systems entirely, this remains one of the most practical migration strategies. Institutions such as Monzo and Starling benefited from building modern stacks from inception, while incumbents increasingly rely on phased modernization approaches to reduce transition risk.

- Leverage Banking-as-a-Service infrastructure: Providers such as Unit and Treasury Prime allow customer-facing experiences to modernize without immediate changes to core systems. While not a long-term substitute for infrastructure transformation, this model enables product delivery to continue while modernization progresses in parallel.

- Prioritize technical debt strategically: For fintech startups, remediation efforts should prioritize debt that directly affects scalability, security, or compliance posture, ahead of issues primarily affecting developer productivity. The challenge severity matrix from Section 2 can help guide prioritization.

Challenge 6: Funding Constraints and the Path to Profitability

What is it?

The capital environment that funded the 2019–2021 fintech expansion no longer exists. VC funding for fintech has declined substantially from peak levels, while investor expectations have shifted toward profitability, capital efficiency, and sustainable growth.

Growth alone is no longer sufficient. Investors are increasingly applying the same financial discipline to fintech companies that they apply to broader software businesses.

Why does it matter more in 2026?

Many fintech companies that raised capital at elevated valuations during 2020 and 2021 are now facing down rounds, extension financing pressure, or operational restructuring.

The funding environment increasingly rewards predictable revenue models, efficient growth, and demonstrable operating leverage.

How to solve it?

Recommended capital strategy measures include:

- Build revenue-oriented operating metrics early: Track LTV:CAC ratio, gross margin by product line, and monthly net revenue retention from launch rather than introducing them reactively during fundraising cycles.

- Pursue regulatory sandbox participation: Beyond operational benefits, participation demonstrates regulatory readiness and reduced compliance risk to investors. Fintech companies with proactive regulator engagement often present lower diligence risk.

- Target fintech-specialized investors: Firms such as Ribbit Capital, QED Investors, and Anthemis possess deeper familiarity with fintech risk models, regulatory environments, and operating dynamics than generalist investors.

- Explore non-dilutive financing pathways: Revenue-based financing providers such as Clearco and Capchase offer alternative funding structures for revenue-generating fintechs. Strategic bank partnerships may also create access to capital through commercial and distribution agreements without equity dilution.

Challenge 7: Customer Acquisition, Retention, and UX Expectations

What is it?

Customer expectations in fintech are increasingly shaped by digital-first financial products, not legacy banking experiences. Users benchmark onboarding speed, interface clarity, real-time notifications, and personalization against market leaders such as Revolut, Robinhood, and Wise.

As a result, fintech companies operating below these experience standards face a measurable competitive disadvantage in both customer acquisition and retention.

Why does it matter more in 2026?

Weak onboarding economics have become increasingly difficult to absorb as acquisition costs rise.

| Customer Acquisition Metric | Typical Range |

| Year-one fintech app churn | 60–70% |

| Customer acquisition cost (CAC) | $100–$200 per customer |

When onboarding performance is poor, elevated churn makes customer acquisition economically inefficient. Replacing customers before they generate meaningful revenue creates sustained pressure on growth efficiency and unit economics.

How to solve it?

Recommended customer retention and UX measures include:

- Implement progressive KYC: Collect only the minimum information required to activate the core product, completing full verification as engagement deepens. Reducing onboarding friction can materially improve Day 1 retention.

- Track activation across key retention windows: Measure Day 1, Day 7, and Day 30 activation independently. These metrics reflect different operational signals:

| Retention Window | Primary Signal |

| Day 1 | Onboarding effectiveness |

| Day 7 | Product-market fit |

| Day 30 | Habit formation and retention |

Strong early activation combined with weak Day 30 retention often signals a product engagement issue rather than an onboarding constraint.

- Invest in personalization capabilities: More mature fintech organizations increasingly tailor notifications, financial insights, and product recommendations based on spending behavior. For earlier-stage companies, behavioral segmentation during onboarding offers a more practical starting point without requiring full ML infrastructure.

Challenge 8: The Talent Shortage in Fintech

What is it?

Fintech operates at the intersection of financial services, software engineering, regulatory compliance, and increasingly machine learning. The talent required to operate effectively across these domains remains limited.

This challenge extends beyond technical capability. Fintech organizations require professionals who can navigate both regulated environments and modern digital infrastructure, a combination that remains difficult to source.

Why does it matter more in 2026?

Demand for professionals with expertise across financial regulation and modern software architecture has grown faster than available supply.

| High-Demand Talent Area | Market Constraint |

| Engineers with fintech and regulatory expertise | Limited talent availability |

| Compliance-aware ML engineers | High compensation premiums |

| Regulated AI specialists | Scarce outside major markets |

The shortage extends beyond engineering functions. Product managers familiar with regulated financial products, fraud analysts capable of working with ML systems, and growth marketers experienced in financial services acquisition constraints remain in limited supply.

How to solve it?

Recommended talent strategy measures include:

- Leverage specialist fintech development partners: Staff augmentation through fintech-focused development firms can provide access to engineers with regulated-industry expertise without the cost and lead time associated with permanent hiring. This approach is particularly effective for project-based requirements such as compliance monitoring systems or legacy modernization initiatives.

- Develop a long-term talent pipeline: Establish relationships with fintech bootcamps, university programs in data science and finance, and industry communities to reduce time-to-hire as workforce requirements expand.

- Benchmark compensation continuously: Salary expectations for fintech-specific roles evolve rapidly. General technology compensation benchmarks often underestimate the premium associated with regulated-industry and compliance-related expertise.

Challenge 9: Embedded Finance and BaaS Dependencies

What is it?

Embedded finance has emerged as one of the fastest-growing fintech segments in 2025 and 2026. The ability to integrate payments, lending, banking, and financial services directly into non-financial platforms has created significant distribution opportunities.

At the same time, this model introduces a distinct category of operational and dependency risk, particularly for fintech companies relying heavily on third-party Banking-as-a-Service (BaaS) infrastructure.

Why does it matter more in 2026?

The 2024 Synapse Financial collapse highlighted the structural vulnerabilities of BaaS dependency. Following Synapse’s bankruptcy, hundreds of fintech companies relying on its middleware infrastructure faced operational disruption and customer fund reconciliation challenges.

| Dependency Risk | Business Impact |

| Single BaaS provider dependency | Operational disruption |

| API reliability failures | Product downtime risk |

| Vendor lock-in | High migration costs |

| Multi-party regulatory structure | Increased compliance complexity |

The incident exposed a broader structural issue: fintech companies relying on a single BaaS provider effectively inherit that provider’s operational, financial, and regulatory risk profile.

How to solve it?

Recommended BaaS risk mitigation measures include:

- Adopt a multi-provider BaaS strategy: Design infrastructure so critical services can route through multiple providers by region or product category, reducing exposure to single-provider failures.

- Establish contractual SLA protections: Service-level agreements with clearly defined uptime commitments and financial penalties improve accountability and operational reliability expectations.

- Evaluate provider financial stability: Due diligence should extend beyond API quality to include financial condition, customer concentration, regulatory relationships, and infrastructure resilience.

- Assess direct licensing pathways: For fintech organizations operating at sufficient scale, obtaining a direct banking license can reduce dependency on intermediary providers while improving operational control and long-term margin economics.

Challenge 10: International Expansion Barriers

What is it?

Fintech products built for a single market often encounter significant structural barriers when expanding internationally. Regulatory licensing, banking partnerships, payment infrastructure, and customer trust typically need to be rebuilt on a market-by-market basis.

International expansion in fintech is rarely a straightforward replication exercise. Operational and regulatory requirements often vary materially across jurisdictions.

Why does it matter more in 2026?

The cost and complexity of market entry have increased as regulatory expectations become more stringent.

| Expansion Constraint | Typical Impact |

| Regulatory licensing | $100,000–$500,000+ in legal and compliance costs |

| US money transmitter licensing | Separate requirements across all 50 states |

| Local banking relationships | 12+ month timelines in some markets |

In the United States, money transmitter licenses (MTLs) are required at the state level, creating fragmented approval requirements and timelines. In parallel, establishing local banking relationships for FBO accounts, IBANs, and settlement rails can significantly delay market readiness where institutional partnerships are not already in place.

How to solve it?

Recommended international expansion measures include:

- Prioritize regulatory compatibility: Market selection should consider regulatory alignment, not just market size. Jurisdictions with similar frameworks allow compliance work to be reused more efficiently.

- Leverage regulatory pathways strategically: Fintech firms with FCA authorization, for example, may access parts of the European Economic Area (EEA) more efficiently through existing regulatory mechanisms than by pursuing entirely separate licensing structures.

- Adopt partnership-led market entry: Working with locally licensed financial institutions or partners can reduce capital requirements and accelerate go-to-market timelines while internal licensing efforts continue.

- Model expansion costs early: Regulatory licensing, legal review, and banking integration costs should be treated as known market-entry requirements during financial planning rather than deferred variables. This reduces capital planning risk and execution delays.

Building Your Fintech Challenge Response Playbook

The severity matrix and challenge descriptions above are only useful if they translate into action.

Here is a prioritization framework for doing that.

Step 1: Audit your current stage. Startups, scaleups, and enterprises each face different challenge clusters. Use the matrix at the top of this guide to identify which challenges are most relevant at your current stage. Focus produces results. Trying to address all ten simultaneously produces none.

Step 2: Map your top three challenges using the severity matrix. For each challenge you identify as high or critical, document the current state, the specific risk or cost it represents, and what “solved” looks like. A challenge without a measurable endpoint stays permanently on the roadmap.

Step 3: Assign ownership. Each challenge needs a named owner. Not a team. Not a department. A person who is accountable for the milestone. Collective ownership of a critical challenge means no one is accountable when the milestone slips.

Step 4: Set a 90-day milestone per challenge. Compliance is never permanently solved. Security is never permanently solved. But each challenge has checkpoints. A 90-day milestone makes the work visible, creates accountability, and forces prioritization of the actions that matter most.

Step 5: Build your external partner stack. You do not need to solve every challenge with internal resources. The partner ecosystem for fintech challenges is mature and specialized.

Here’s the tool stack recommendations to tackle various challenges on your fintech platform –

| For regulatory and compliance technology | ComplyAdvantage and Flagright for AML and transaction monitoring. |

| For fraud and security | Feedzai and Sardine for real-time fraud detection. For KYC and KYB: Jumio and Onfido for identity verification. |

| For BaaS infrastructure | Unit and Treasury Prime for embedded banking, with multi-provider architecture from the start. |

| For technical talent | specialists, fintech development firms for staff augmentation in infrastructure and compliance engineering. |

Building or modernizing a fintech platform often requires coordinated expertise across compliance-sensitive architecture, API integrations, secure payment infrastructure, KYC/KYB workflows, real-time data systems, and user experience optimization. Execution gaps at the integration layer frequently become bottlenecks for scalability, regulatory readiness, and time-to-market.

In this regard, Simpalm brings expertise as a trusted fintech development partner supporting businesses through secure and compliant-from-day-1 platform engineering, regulated workflow implementation, fintech API integrations, and scalable mobile and web application development.

Expert fintech developers at Simplam help:

- Modernizing legacy infrastructure

- Building embedded finance capabilities,

- Strengthening onboarding, KYC, and ID verification flows,

- Developing end-to-end fintech platforms, including websites and dedicated apps.

Moreover, the company emphasizes creating systems that are secure, compliant, and aligned with measurable business outcomes.

Conclusion

Fintech challenges in 2026 are not temporary market disruptions or isolated operational issues. They reflect the structural realities of operating in an industry defined by regulatory scrutiny, security expectations, capital efficiency, and accelerating technological change. As fintech matures, the complexity of building resilient, scalable financial products continues to increase.

The organizations most likely to sustain long-term growth are not those attempting to eliminate every challenge at once. They are the ones who understand their risk profile, stage-specific constraints, and regulatory obligations, then prioritize investments accordingly.

In practice, competitive advantage in fintech industry comes from building systems where compliance, security, infrastructure resilience, and customer experience function as integrated operational capabilities rather than reactive fixes.

Frequently Asked Questions

Q1. What are the most common fintech challenges in 2026?

Ans. The most common fintech industry challenges are regulatory compliance across multiple jurisdictions, cybersecurity and fraud threats, AI-related risks in automated decision-making, rising costs of third-party APIs, legacy technology constraints, funding and profitability pressure, customer acquisition and retention, talent shortages, BaaS and embedded finance dependencies, and international expansion barriers.

Q2. How do fintech startups manage regulatory compliance without large legal teams?

Ans. Early-stage fintechs manage compliance through a combination of compliance-by-design architecture, RegTech tools that automate monitoring and reporting, regulatory sandbox participation in their primary market, and dedicated compliance engineering. The goal is to build compliance into the product rather than treating it as a separate function.

Q3. What is the biggest challenge in the fintech industry that most companies overlook?

Ans. AI-specific risks are the most consistently unaddressed challenge in fintech. While AI is widely discussed as a solution, the regulatory exposure from algorithmic bias, the compliance requirements of the EU AI Act for high-risk AI systems, and the operational risk of deploying models that cannot produce explainable outputs receive far less attention than they deserve.

Q4. How do fintech companies protect against cybersecurity threats?

Ans. The foundational approach is zero-trust architecture, combined with AI-powered fraud detection, deepfake-resistant KYC verification, regular penetration testing, and compliance certifications including PCI DSS, SOC 2, and GDPR. For companies relying on third-party infrastructure, vendor security posture is also a critical part of the overall security model.

Q5. What is the best way to prioritize fintech challenges when resources are limited?

Ans. Start with a challenge severity matrix calibrated to your company stage. Identify the two or three challenges that represent the highest near-term risk to revenue, regulatory standing, or operational continuity. Assign named owners and 90-day milestones. Build your external partner stack for areas where specialist tools and firms offer faster progress than internal development.