Digital wallets have become a core part of how modern transactions happen. From everyday purchases to saving boarding passes, ID cards, and event tickets, they have become a big part of our lives. From groceries and utility payments to airport check-in, users increasingly expect everything to be handled seamlessly through their mobile devices. This shift is not only changing consumer behavior but also reshaping how businesses think about payments, loyalty, travel, and customer engagement.

As adoption grows, more companies are exploring how to build their own digital wallet solutions instead of relying entirely on third-party platforms. But developing a digital wallet is a complex process that goes far beyond basic payment integration to storing documents, boarding passes, and event tickets. It involves defining the right feature set, choosing a scalable technology stack, ensuring strong security measures, and complying with financial regulations.

This guide breaks down everything you need to know about digital wallet app development in 2026, including features, development process, cost considerations, and security and compliance requirements. Let’s start by understanding the digital wallet app and how it works!

What is a Digital Wallet App?

A digital wallet app is a mobile application that lets users store, manage, and use a wide range of digital assets in one place. Think of it as a virtual version of your physical wallet, except it holds far more than cash and cards.

A modern digital wallet can store:

- Payment methods (debit cards, credit cards, bank accounts)

- Boarding passes and travel documents

- Event and concert tickets

- Loyalty and rewards cards

- Membership and subscription passes

- Government IDs, driver’s licenses, and health cards

- Hotel key cards and office access credentials

- Coupons, gift cards, and promotional vouchers

Users can pay at stores, send money to friends, scan a QR code at a stadium gate, show a digital ID at security, or tap their phone to unlock a hotel room, all from a single app.

How a Digital Wallet Actually Works: The Technical Flow

Here is what happens behind the scenes when someone uses their digital wallet, whether to pay, present a pass, or verify their identity:

For Payments

- The user opens the app and selects the relevant card, pass, or credential.

- The app generates a secure token or encrypted data package.

- That token is transmitted to a reader, gateway, or verifier via NFC, QR code, or BLE.

- The receiving system validates the token against its backend.

- The transaction, entry, or verification is approved or rejected.

- The user sees a success or failure message in real time.

For payments, this entire flow takes 1 to 3 seconds. Real card data never travels to the merchant. For passes and credentials, the same principle applies: sensitive data is never exposed in its raw form.

For Boarding Passes/Event Tickets

- The user adds a boarding pass, movie ticket, or event pass to the wallet via app integration, email link, QR scan, or direct issuer issuance.

- The wallet stores a structured pass object provided by the issuer, including key details such as identity, booking or seat information, event metadata, and a machine-readable barcode or QR code.

- When the user arrives at the airport, venue, or entry gate, they open the pass inside the wallet.

- The wallet renders the barcode or QR code on screen, which may be static or dynamically refreshed depending on the issuer’s system.

- The scanner at the gate reads this code and sends it to the issuer’s backend system for validation.

- The backend verifies authenticity, validity window (date/time), seat or allocation details, and whether the ticket has already been used.

- If valid, the entry is approved instantly; if not, it is rejected with an error such as expired, invalid, or already redeemed.

- The wallet updates the pass status in real time, showing states like “Checked In,” “Boarded,” or “Used.”

For tickets and boarding passes, security is primarily enforced through issuer-controlled barcode/QR validation, with some systems adding signatures, encryption, or rotating codes for additional protection.

Digital Wallet Market: Size, Growth, and the Business Case

The digital wallet space is growing faster than most people realize.

The global digital payments market was valued at over $111 billion in 2023 and is projected to cross $450 billion by 2032. Mobile wallet transactions are predicted to hit $12 trillion globally by 2027. But payments are only part of the picture. Digital ID programs are being rolled out at a national scale across the EU, US, Australia, and India.

What is Driving Mass Adoption in 2025–2026

- Smartphones are now in the hands of over 6 billion people globally.

- Contactless behavior accelerated sharply after the COVID-19 pandemic and never reversed.

- Airlines, stadiums, hotels, and transit systems have moved aggressively to mobile-first credential systems.

- Gen Z and Millennials expect everything, from concert access to car rental, to happen through their phone.

- Governments are issuing digital IDs and health credentials that feed directly into wallet apps.

Why Digital Wallets are getting popular?

Digital wallets are gaining popularity because they combine payments, tickets, passes, and identity in one secure, easy-to-use app. They enable fast, contactless transactions, reduce reliance on physical cards, and improve security through encryption and tokenization. With growing smartphone adoption and ecosystems like Apple Wallet and Google Wallet, they are becoming a central tool for everyday digital transactions.

Types of Digital Wallet Apps You Can Build

Before you start building, you need to know which type fits your goal. The use case you are solving for determines everything, from the features you build to the compliance you need.

Here are some of the most common types of digital wallet apps you can build –

Closed Wallets (Single Brand or Merchant): These wallets only work within one brand’s ecosystem. The Starbucks app is the classic example: load money in, spend it only at Starbucks. Many loyalty and membership wallets fall into this category. These are the easiest to build and have the lowest compliance overhead.

Semi-Closed Wallets (Multi-Merchant, Single Operator): These wallets work across many merchants or partners but are run by one company. Paytm and PhonePe are examples. Users can pay at thousands of locations, but the wallet stays tied to one platform operator.

Open Wallets (Bank-Linked, Full Financial Access): These are the most complex. They allow withdrawals, transfers to any bank, and payments anywhere. They require a banking license or a partnership with a licensed financial institution.

Pass and Credential Wallets: These wallets focus on storing and presenting non-payment credentials, including tickets, boarding passes, hotel keys, gym memberships, and loyalty cards. Apple Wallet and Google Wallet operate largely in this space. Apps can integrate directly with these platforms or build proprietary pass management systems.

Identity and Document Wallets: A growing category. These wallets store verified digital identities, driver’s licenses, health cards, or professional certifications. They use cryptographic verification to prove authenticity without exposing the underlying document. Several governments are now building standards for this.

Cryptocurrency Wallets: These store crypto assets like Bitcoin or Ethereum and need strong encryption along with blockchain-based transaction support. Building one requires deep expertise in blockchain infrastructure and key management.

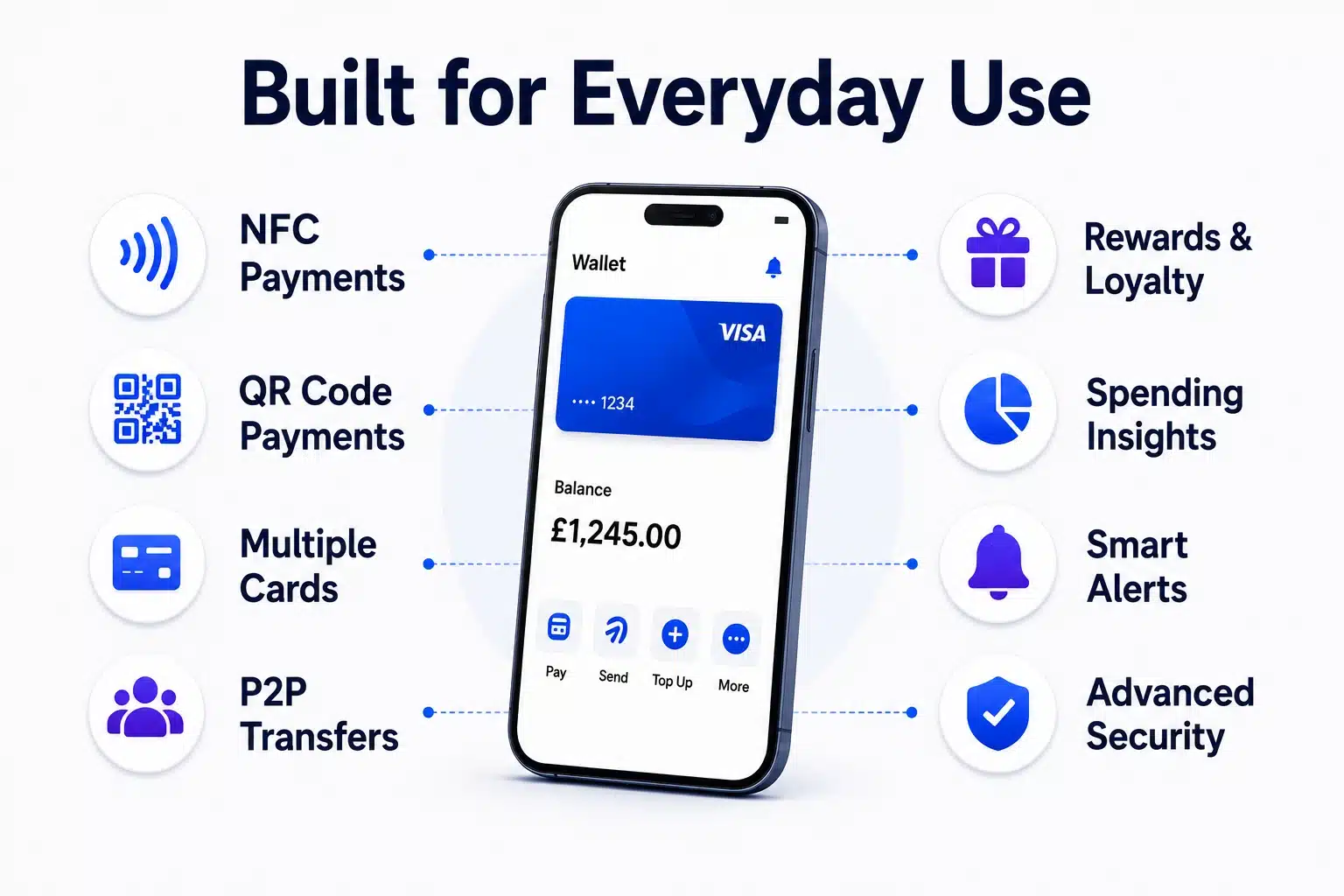

Must-Have Digital Wallet App Features for Modern Products

Getting the features right is the most critical part of wallet development.

The right feature set depends heavily on your wallet type, but here are the core capabilities that modern wallets are expected to deliver.

- User Onboarding and Identity Verification: Users need to sign up and verify their identity. For payment wallets, this is called KYC (Know Your Customer) and involves collecting a government ID, selfie, and sometimes address proof. For pass-and-credential wallets, onboarding typically means linking existing accounts (airline frequent flyer, gym membership, event booking). Either way, the sign-up flow needs to be fast, clear, and frictionless.

- Wallet Storage: Cards, Passes, and Credentials: The core of any wallet is its storage layer. For payment wallets, this means linking bank accounts, storing card details securely, and enabling top-ups. For broader wallets, it means organizing all the passes, tickets, IDs, and loyalty cards a user holds, displayed clearly so the right one is always one tap away.

- Payment Processing: QR Code, NFC, and In-App Checkout: In-store payments use either QR codes (scan and pay) or NFC (tap and pay). In-app and online checkout flows complete the picture. All three need to be integrated tightly with your payment processor and tested across devices.

- Pass Management: Boarding Passes, Tickets, and Memberships: This is one of the most underbuilt areas in custom wallet apps. Users expect their passes to update automatically, for example when a gate changes, a flight is delayed, or an event is rescheduled. Real-time push updates, expiry management, and barcode rendering are all non-negotiable for a good pass experience.

- Peer-to-Peer (P2P) Transfers: One of the most-used features in payment wallets. Users send money to friends or family using a phone number, email, or QR code. Speed and reliability matter above everything else here.

- Loyalty, Rewards, and Points Management: Loyalty programs are a core wallet feature, not an add-on. Users accumulate points, redeem rewards, and track tier status directly inside the app. A well-built loyalty layer dramatically increases engagement and return visits.

- Transaction and Activity History: Users want to see a full record of everything that has happened in their wallet, payments made, passes used, rewards earned, and credentials presented. Clean history with filters, categories, and export options builds trust and keeps users engaged.

- Push Notifications and Smart Alerts: Every time something moves, whether money, a pass, or a credential update, users expect to be notified. Alerts for payments received, gate changes, expiring passes, low balance, and suspicious activity are all standard. Timely, relevant notifications are what make a wallet feel alive rather than static.

- Multi-Currency and Cross-Border Support: If your users are global, your wallet needs to handle multiple currencies with real-time exchange rates, conversion fees, and international transfer rails. For travel wallets in particular, seamless currency handling is a table-stakes feature.

AI-Powered Features Redefining Digital Wallets in 2026

AI is no longer a bonus feature in wallet development. It is becoming the baseline expectation for any wallet that wants to stand out.

- Fraud Detection and Anomaly Alerts: Machine learning models monitor every transaction and credential presentation in real time. If a payment looks unusual, or if a credential is being used from an unexpected location or device, the system flags it instantly. This reduces fraud without creating unnecessary friction for legitimate users.

- Personalized Spend Insights and Budgeting Recommendations: AI analyzes spending patterns and offers genuinely useful nudges. “You spent 30% more on dining this month.” “You are on track to hit your savings goal.” These insights improve retention because they make the wallet feel like a financial advisor, not just a tool.

- Smart Pass and Credential Organization: AI surfaces the right card, pass, or credential at the right time. If a user has a flight in two hours, their boarding pass should appear at the top of the wallet automatically. If they are at a coffee shop they visit every morning, their loyalty card should be the default. This contextual intelligence is a major differentiator.

- AI-Based Transaction Categorization: Instead of users manually tagging transactions, AI sorts them automatically into categories: groceries, transport, entertainment, travel. This happens without any effort from the user and makes spending history far more useful.

- Conversational Payment and Wallet Assistants: Some wallets now allow users to interact via voice or chat. “Send $50 to Alex,” “Show my boarding pass,” or “How many loyalty points do I have?” are all handled by an AI assistant inside the app. This reduces friction for power users and helps new users discover features they would never find by browsing.

- Predictive Cash Flow Analysis for Business Wallets: For business-facing wallets, AI can predict upcoming cash needs based on historical patterns, flagging potential gaps before they become problems. This is particularly valuable for freelancers and small business operators.

Digital Wallet Security: Architecture and Best Practices

Security is not something you add at the end. It must be built into the architecture from the very first design decision.

Tokenization and Encryption Standards

Real card numbers, credential data, and personal IDs are never stored in their raw form. They are replaced with secure tokens, random strings that are meaningless to anyone who intercepts them. All data in transit and at rest is encrypted using AES-256 or higher standards.

Multi-Factor Authentication and Biometric Verification

Users verify their identity in more than one way. This means a password plus a fingerprint, face scan, or one-time code. Biometric login is now the expected standard for wallet apps. For credential presentation (digital ID, access passes), biometric confirmation before display adds an important layer of protection.

Secure Element and TEE (Trusted Execution Environment)

Payment credentials and sensitive passes are stored in a secure chip (Secure Element) on the device or inside a protected processor zone (TEE). This makes it nearly impossible to extract credential data even if the device is compromised.

Fraud Monitoring and Real-Time Risk Scoring

Every transaction and credential event gets a risk score based on factors including device fingerprint, location, time, amount, and behavior history. High-risk events trigger extra verification or block the action automatically.

Security Testing Checklist Before Launch

Every wallet app should pass through all of the following before going live:

- Penetration testing (ethical hacking to find exploitable gaps)

- OWASP Mobile Security Testing Guide compliance checks

- SSL/TLS certificate audit

- Full code review for vulnerabilities

- Third-party API and SDK security assessment

Regulatory Compliance for Digital Wallet Apps

Compliance is one of the hardest challenges in wallet development. It is also one of the most frequently underestimated.

KYC and AML Requirements

Every payment wallet must verify user identities (KYC) and monitor for suspicious activity (AML, Anti-Money Laundering). Failure to comply results in heavy fines or forced shutdowns.

PCI-DSS Compliance for Card Data Handling

If your wallet stores, processes, or transmits card data, you must comply with PCI-DSS standards. These are strict security rules enforced by the major card networks.

Credential and Identity Wallet Standards

For wallets that store digital IDs or government-issued credentials, compliance is governed by emerging frameworks including ISO/IEC 18013-5 (for mobile driver’s licenses), W3C Verifiable Credentials standards, and country-specific identity authority requirements. This space is evolving quickly in 2026 and requires careful monitoring.

Key Notes on Regional Payment Regulatory Scenario

The rules differ significantly by region:

| Region | Key Regulation | Notes |

| EU | PSD2, GDPR | Open banking access + strong authentication |

| US | FinCEN MSB Registration | Required for most wallet operators |

| UK | FCA Authorization | Required for e-money and payment services |

| India | RBI PPI Guidelines, NPCI UPI approval | Required for UPI-based wallets |

GDPR and Data Privacy Obligations

If you serve users in Europe, GDPR applies. Users have the right to see, delete, and control their data. Your app needs a clear privacy policy, consent management, and data storage controls built into the architecture, not bolted on later.

How to Build Compliance Into Architecture From Day One? The smartest approach is to think about compliance before writing the first line of code. Choose infrastructure partners that are already certified. Pick KYC vendors with established audit trails. Build access logs and data residency controls into your database schema from the start. Fixing compliance gaps after launch costs five times more than designing for them upfront.

Technology Stack for Digital Wallet App Development

| Development Layer | Technologies | Description |

| Mobile & Web Frontend | iOS: Swift / React

Android: Kotlin / React NativeWeb: React.js / Vue.js |

React Native is commonly used for cross-platform development, enabling a single codebase for both iOS and Android, reducing development time and maintenance costs. |

| Backend Infrastructure & API Layer | Node.js / Python (Django, FastAPI)GraphQL / REST APIsMicroservices Architecture | Handles core business logic, API communication, and scalable system design. Microservices allow independent scaling of features like payments, KYC, and notifications. |

| Database, Cache & Real-Time Processing | PostgreSQL / MySQLRedisKafka / RabbitMQ | Stores transaction data, manages caching for fast access, and processes real-time event queues for high-volume financial operations. |

| Payment Gateway & Banking Integrations | Stripe / Razorpay / BraintreePlaid / YodleeTwilioNPCI APIs | Enables secure payment processing, bank account linking, OTP authentication, and UPI-based transactions (especially for India). |

| Pass & Credential Integrations | Apple Wallet (PassKit)Google Wallet APICustom Pass Servers | Used for issuing and managing digital passes such as tickets, loyalty cards, and branded wallet experiences. |

| Cloud, Security & DevOps Layer | AWS / Google Cloud / AzureDocker / KubernetesHashiCorp VaultCloudWatch / Datadog | Provides scalable infrastructure, container orchestration, secrets management, and system monitoring for reliability and security. |

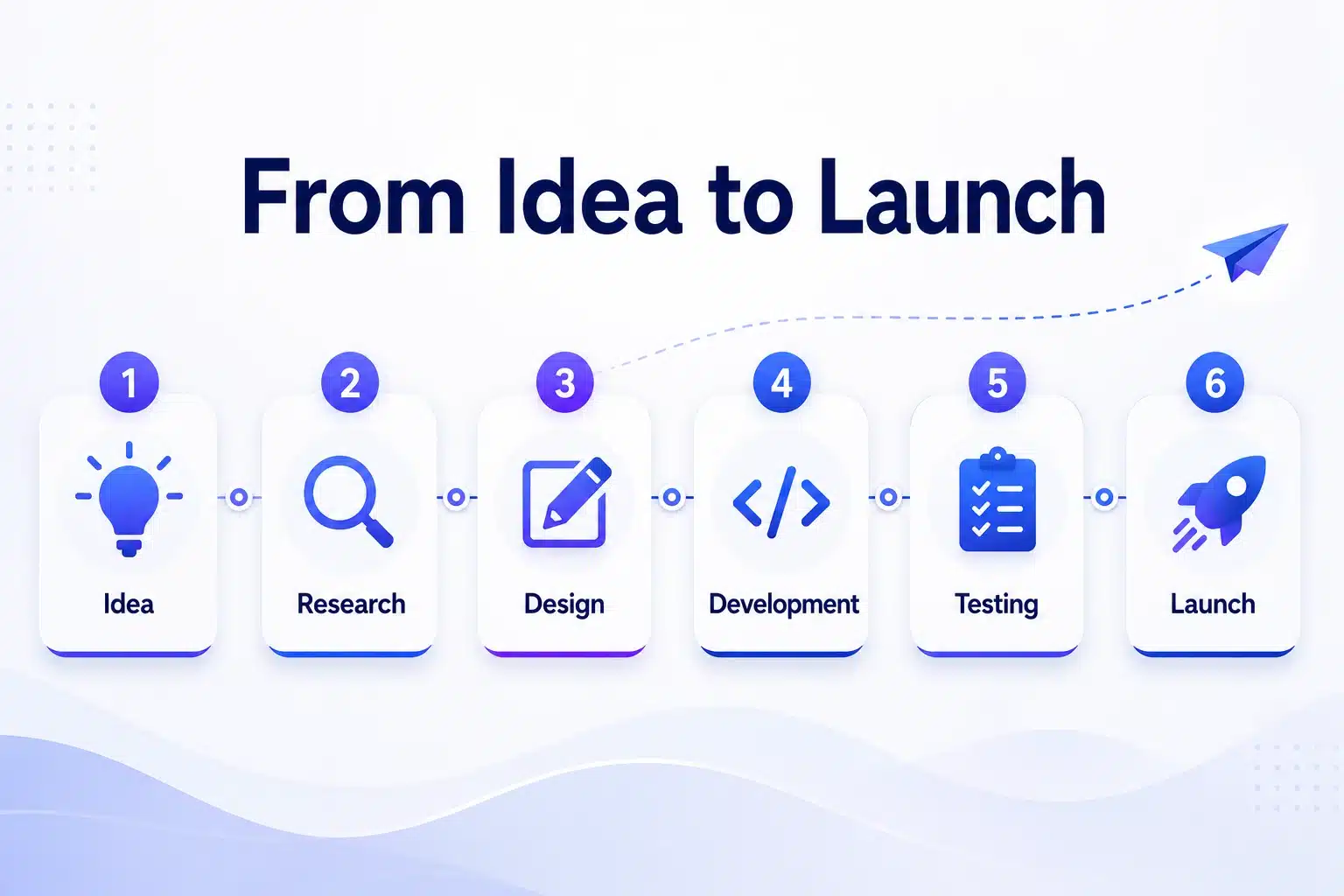

Step-by-Step Digital Wallet App Development Process

Here is how a professional team builds a wallet app from concept to launch.

Step 1: Define Wallet Type, Use Cases, and Compliance Requirements

Decide what your wallet is for: Payments only? Passes and tickets? Digital identity? A combination? This decision determines your compliance obligations, technology choices, and development timeline.

Step 2: Market Research and MVP Scoping

Study your target users. What problem does your wallet solve that existing apps do not? What is the smallest version that delivers real value? Avoid building everything at once.

Step 3: UX Wireframing and User Flow Design

Map every screen from sign-up to first successful use. Good wallet UX reduces drop-offs, especially at onboarding and verification. Financial and credential apps need to feel trustworthy and clear, not clever.

Step 4: UI Design and Design System

Build a visual design system with consistent colors, fonts, and components. Prioritize simplicity. Users are trusting your app with their money, their identity, and their travel documents. The UI needs to earn that trust.

Step 5: Frontend and Backend Development

Build core flows first: sign-up, wallet setup, and the primary use case (payment or pass). Add secondary features after the core is stable.

Step 6: Third-Party API and Integration Work

Connect your KYC provider, payment processor, bank linking tools, and pass issuance APIs. Test every integration thoroughly in sandbox mode before touching real data.

Step 7: Security Audit and Penetration Testing

Hire an independent security firm to test the app before launch. For any wallet holding financial data or identity credentials, this step is not optional.

Step 8: QA, Load Testing, and Compliance Review

Test every user flow end to end. Simulate high transaction and event volumes to find performance bottlenecks. Get a compliance review from a legal expert who knows your target markets.

Step 9: App Store Submission and Soft Launch

Submit to the App Store and Google Play. Financial and identity apps face stricter review processes, so allow extra time. Run a soft launch with a limited group before opening to everyone.

Step 10: Post-Launch Monitoring and Iteration

Launch is not the finish line. Monitor KPIs closely, fix bugs fast, and keep improving based on real user feedback.

How much does Digital Wallet App Development Cost?

The cost of building a digital wallet depends on the complexity of the use case, the number of platforms, and the team you use to build it.

Average Cost by Wallet Type and Complexity

| Wallet Type | Estimated Cost |

| Basic (Closed Wallet / MVP) | $20,000 – $50,000 |

| Mid-Level (Semi-Closed, P2P, or Pass Wallet) | $50,000 – $150,000 |

| Enterprise (Open Wallet, Full Features, Identity) | $150,000 – $500,000+ |

Key Factors That Drive Development Cost Up or Down

- Number of platforms: iOS + Android + Web costs more than a single platform.

- Wallet scope: Adding identity, passes, and loyalty on top of payments adds significant development time.

- Compliance complexity: Multi-country regulatory requirements add both legal and technical overhead.

- AI features: Machine learning integration adds cost upfront but delivers long-term value.

- Custom design: Unique UI costs more than using existing component libraries.

- Third-party integrations: Each additional API adds development and testing time.

Comparing Cost Effectiveness: In-House vs. Outsourced vs. Development Agency

- In-house team: Highest upfront cost ($300K–$700K/year in salaries). Best for long-term products with continuous development needs.

- Freelancers: Cheapest option but risky for security-critical and compliance-heavy apps. Coordination overhead is significant.

- Development agency: Best balance of cost, speed, and expertise for most projects. Agencies with fintech and mobile experience bring pre-built components that reduce timeline significantly.

How Businesses Can Monetize a Digital Wallet App

Building the app is one thing. Making it a profitable business is another.

- Transaction Fees and Interchange Revenue: Charge a small fee on P2P transfers, currency conversion, or merchant payments. Even 0.5–1.5% per transaction adds up at scale.

- Subscription Plans and Premium Tier Features: Offer a free base plan and a paid premium tier. Premium features could include higher transfer limits, faster payouts, priority customer support, or advanced spending analytics.

- Pass Issuance and Credential Management Fees: If your wallet supports third-party pass issuance, charge businesses a fee per pass issued or a monthly platform access fee. Airlines, event organizers, hotels, and gyms all need a reliable way to push passes to their customers.

- Merchant Onboarding Fees and Commission: If merchants use your wallet as a payment method or loyalty platform, charge an onboarding fee or a commission on sales processed through your platform.

- Value-Added Financial Services: Once you have an active user base, you can offer complementary financial products: personal loans, micro-insurance, or investment options. These carry high margins and deepen user loyalty significantly.

- In-App Advertising and Partner Promotions: Let merchants and partners promote cashback offers or targeted deals directly inside your wallet. Users get relevant discounts; you earn a promotion fee. This model works especially well for high-traffic consumer wallets with strong location and behavioral data.

Common Challenges in Digital Wallet Development and How to Solve Them

Building a digital wallet is hard. Here are the most common problems teams run into and the practical fixes.

Real-Time Reliability at Scale

When thousands of transactions and pass validations happen simultaneously, systems can slow down or fail. The fix: use a message queue system (like Kafka), auto-scaling cloud infrastructure, and stress-test before launch.

Keeping Passes and Credentials in Sync

When a flight gate changes or an event is rescheduled, every affected pass needs to update immediately. The fix: build a real-time push notification layer tied directly to your pass management backend. Stale passes destroy user trust faster than almost anything else.

Regulatory Complexity Across Geographies

Every country has different rules for payments, identity, and data storage. Trying to comply with all of them at once is overwhelming. The fix: launch in one market first. Get compliance right there before expanding.

User Trust and Adoption Barriers

People are cautious about new apps that hold their money, tickets, and IDs. The fix: invest in social proof early, security certifications displayed prominently, clear privacy language, and real user testimonials. Show users exactly how their data is protected.

Third-Party API Dependency Risk

If your payment gateway or pass issuance API goes down, your entire app stops working. The fix: build fallback processors and maintain secondary integrations. Never depend entirely on a single third-party API for a critical function.

Fragmented Device and OS Compatibility

Wallets that rely on NFC, biometrics, or Secure Element features behave differently across Android models and iOS versions. The fix: test on a wide device matrix before launch and budget for OS compatibility updates every cycle.

Post-Launch Maintenance and Growth Strategy

Launching your wallet app is a milestone. The real work begins after.

KPIs to Track After Launch

- Monthly Active Users (MAU)

- Transaction and pass usage success rate (aim for 99.5%+)

- Pass add rate (how many users add a non-payment card within 30 days)

- User retention at 30 and 90 days

- Customer acquisition cost vs. lifetime value

Other Post-launch Optimizations to Integrate

Ongoing Security Patching and OS Compatibility: New Android and iOS updates ship every year. Each one can break NFC behavior, biometric flows, or push notification handling. Budget for a dedicated engineering resource to handle updates and security patches monthly.

User Feedback Loops and Feature Prioritization: Use in-app surveys, app store reviews, and customer support tickets to understand what users actually want next. Build what solves real problems, not what looks impressive on a product roadmap.

Scaling Infrastructure for Volume Growth: As your user base grows, your infrastructure needs to scale with it. Kubernetes auto-scaling, CDN optimization, and database sharding help handle millions of daily events without degradation.

How to Choose the Right Digital Wallet Development Company

Your development partner can make or break this project. Here is what to look for and what to avoid.

Key Qualities to Look For

- Fintech and mobile experience: Have they built payment, identity, or pass-management apps before? Ask for case studies with real project details.

- Security expertise: Do they follow OWASP standards? Do they conduct independent security audits before launch?

- Compliance knowledge: Do they understand the regulations relevant to your market and wallet type?

- Post-launch support: Will they maintain and update the app after launch, or do they hand off and disappear?

Red Flags to Avoid

- Agencies promising to build a full-featured wallet in four weeks for $5,000

- Teams with no portfolio in financial, identity, or regulated-industry apps

- No mention of security audits or compliance in their development process

- Poor communication during the sales process (this always gets worse during development)

Questions to Ask Before Signing a Contract

- Can you show me a completed digital wallet or fintech project?

- How do you approach compliance for my target market?

- What security testing do you conduct before launch?

- How do you handle post-launch support and OS compatibility updates?

- What does your process look like when scope changes or timelines shift?

Ready to Build Your Digital Wallet App?

Building a digital wallet is a serious investment. It takes the right plan, the right team, and a clear understanding of your users before you write a single line of code.

Before moving forward, make sure you have clear answers to these questions:

- What type of wallet are you building: payments, passes, identity, or a combination?

- Which market are you launching in first, and what compliance requirements apply there?

- What is your MVP, the smallest version that solves a real, specific problem for users?

- How will your wallet generate revenue in the long run?

- Who will build and maintain it, and do they have genuine fintech and mobile experience?

Get these right upfront, and you save months of rework and significant avoidable cost down the road.

If you are ready to take the next step, the team at Simpalm can help. Simpalm is an experienced fintech and mobile app development company that has built secure, scalable payment, pass management, and wallet applications for startups and enterprise clients alike. From scoping your MVP to handling compliance and post-launch support, they cover the full journey.

Reach out to Simpalm today to discuss your digital wallet idea and get a free project estimate.

Get in touch!

Final Thoughts

Digital wallets are no longer just a payment tool. They are becoming the primary way people carry and present everything of value in their daily lives: money, yes, but also access passes, identity documents, loyalty memberships, event tickets, and travel credentials. For businesses, this represents an opportunity to build deeper, more durable relationships with users, reducing transaction costs while creating new touchpoints across the entire customer journey.

That said, a digital wallet is a regulated, security-sensitive product regardless of whether it handles money, identity, or both. It demands careful planning, a scalable architecture, and a disciplined approach to compliance. Small gaps in security or regulatory coverage create outsized consequences.

The most successful digital wallet products are those that think beyond the single use case. They are built to grow from a loyalty card holder into a full lifestyle wallet, or from a payment tool into a trusted identity layer. They earn user trust through reliability, security, and genuine usefulness, and they evolve continuously as new use cases emerge and new regulations take shape.

Frequently Asked Questions

Q1. How long does it take to build a digital wallet app?

Ans. A basic MVP takes 3–5 months. A full-featured wallet with payments, pass management, compliance, and AI features across multiple platforms typically takes 8–14 months.

Q2. Can a digital wallet store both payment cards and non-payment passes?

Ans. Yes. Modern wallet apps are designed to handle multiple credential types in a single unified experience. You can build a wallet that stores cards, tickets, loyalty passes, and digital IDs side by side.

Q3. Do I need a license to launch a digital wallet?

Ans. It depends on the wallet type and your market. Closed wallets and pass-only wallets have the lowest licensing requirements. Open wallets that handle withdrawals or bank transfers almost always require a license or a banking partner. Identity wallets are subject to evolving standards depending on the country.

Q4. Is it cheaper to build a wallet in India than in the US?

Ans. Yes. Development agencies in India offer high quality at 40–60% lower cost compared to US or Western European agencies. Many global fintech products, including payment and wallet apps, are built by Indian development teams.

Q5. What is the minimum budget to build a digital wallet app?

Ans. A basic MVP-level wallet starts at around $20,000–$30,000. Going below that usually means skipping security testing or compliance architecture, which creates much larger problems and costs later.

Q6. What is the difference between a pass wallet and a payment wallet?

Ans. A payment wallet handles financial transactions: sending money, paying merchants, and linking bank accounts. A pass wallet stores and presents non-payment credentials like boarding passes, event tickets, membership cards, and hotel keys. Many modern wallet apps combine both in a single product.